PAN Bill In Nepal – Format – Limit – Rules And Free Sample – 2026

If you run a business in Nepal and you are not registered for VAT, you issue a PAN Bill – also called a PAN invoice or PAN Bill.

But most business owners have Questions – How much can I bill through PAN? What should be on the bill? When must I switch to VAT? What is the fine if I do not issue one?

This guide answers all of those questions in plain language – based directly on Nepal’s Value Added Tax Act 2052, VAT Regulations (Rule 56) and Income Tax Act 2058.

Also Helpful: Personal PAN Card Registration In Nepal

What Is A PAN Bill In Nepal?

PAN stands for Permanent Account Number. A PAN bill is a legal transaction document issued by a business or individual that is registered under PAN but not under VAT.

In Simple Terms: if your business is too small to require VAT registration, you use a PAN bill for every sale. It acts as legal proof of the transaction for income tax purposes under the Income Tax Act 2058.

Key Point: A PAN bill does NOT include VAT (13%). It is a simple invoice showing the transaction amount without any added tax. VAT is only on bills issued by VAT-registered businesses.

Who Issues A PAN Bill In Nepal?

Any individual or business that is:

- Registered with a PAN number at the Inland Revenue Department (IRD).

- NOT registered for VAT (meaning annual turnover is below the VAT threshold).

- Conducting taxable transactions – selling goods or providing services.

This typically includes small shops, freelancers, consultants, traders and service providers whose annual business income is below Nepal’s VAT registration threshold.

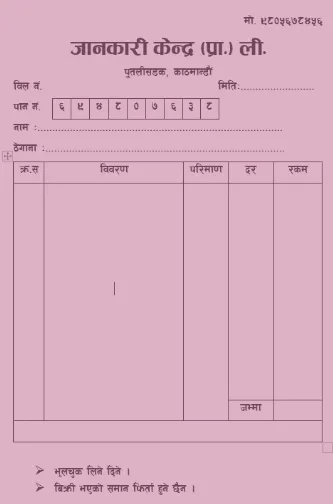

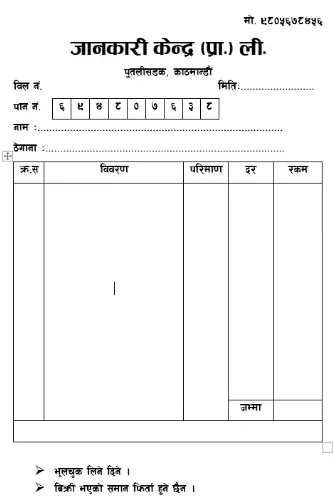

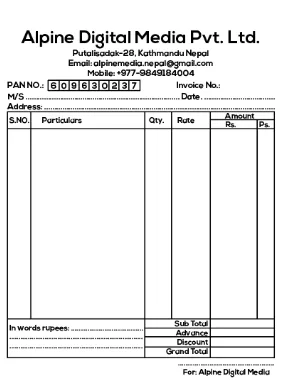

PAN Bill Format – What Must Be Included

Nepal’s Inland Revenue Department does not prescribe a single fixed template for PAN bills, but there are mandatory fields that every PAN bill must contain to be legally valid.

| Required Field | Details / Example |

| Seller’s Full Name | The business or individual name as registered with IRD |

| Seller’s PAN Number | Your 9-digit PAN number (e.g. 123456789) |

| Business Address | Full registered address of the seller |

| Bill Number | Sequential invoice number (e.g. 001, 002 – must not repeat) |

| Bill Date | Date of transaction in BS (Bikram Sambat) format |

| Buyer’s Name | Name of the person or business purchasing |

| Description of Goods/Services | Clear description of what is being sold or provided |

| Quantity and Rate | Number of units and price per unit |

| Total Amount | Final amount in Nepali Rupees (no VAT added) |

| Signature | Authorized signature of the seller or representative |

Important: PAN bills must be serially numbered. Skipping numbers, repeating numbers or issuing unnumbered bills is a compliance violation. Keep a physical or digital copy of every bill issued.

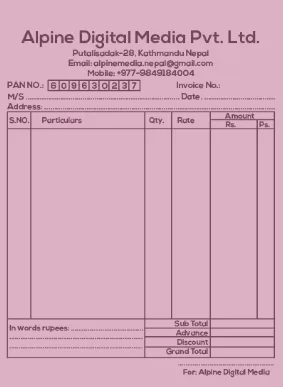

PAN Bill Format In Nepal – Design Requirements

While no single government-mandated template exists, your PAN bill design should:

- Clearly display your PAN number at the top or in the header.

- Show the business name prominently.

- Include a unique bill number on every invoice.

- Be printed or written clearly – handwritten bills are acceptable.

- Not include any VAT amount or VAT number (since you are not VAT-registered).

PAN Bill Transaction Limit In Nepal

This is the most misunderstood topic in Nepali business taxation. The short answer is – there is no fixed maximum amount per PAN bill transaction.

You can issue a PAN bill for NRs. 5,000 or NRs. 5 lakh – the amount per bill is not restricted. What is restricted is your total annual turnover. Here is how the threshold works:

| Business Type | Annual Turnover Limit for PAN Bill | What Happens After Limit |

| Goods / Products | Up to NRs. 50 lakh (NRs. 5,000,000) | Must register for VAT and issue VAT bills |

| Services | Up to NRs. 20 lakh (NRs. 2,000,000) | Must register for VAT and issue VAT bills |

| Mixed (Goods + Services) | Depends on taxable goods portion | Assessed separately – consult IRD |

Example: If you are a goods trader and have already billed NRs. 45 lakh this year and a new customer wants to buy NRs. 8 lakh worth of goods – that single transaction will push you over NRs. 50 lakh. At that point, you cannot issue a PAN bill. You must first register for VAT and then issue a VAT Bill for that transaction.

Practical Rule: Watch your cumulative annual turnover, not the amount per bill. One bill can be any amount – but once your total annual turnover crosses the VAT threshold, you must switch to VAT billing.

NRs. 20,000 Rule In Pan Bill In Nepal

Many business owners in Nepal have heard the rumor that “You Cannot Issue A PAN Bill Above NRs. 20,000.” This is a common misconception.

Here Is The Truth: VAT Regulation Rule 56 states that government bodies – including local governments (Palika), provincial governments and federal government offices – are required to purchase goods or services worth more than NRs. 20,000 only from VAT-registered suppliers.

This NRs. 20,000 rule applies ONLY to government procurement. It does NOT apply to private businesses or individual transactions. If you are selling to a private customer, you can issue a PAN bill for any amount – as long as your total annual turnover stays within the VAT threshold.

This rule was historically used by businesses to split large government orders into multiple bills of under NRs. 20,000 – a practice that is now tracked and penalized by the IRD.

TDS On PAN Bills In Nepal

TDS stands for Tax Deducted at Source . TDS may apply to certain payments even when the supplier is only PAN-registered.

Under Nepal’s Income Tax Act 2058, specific types of payments require the paying party to deduct TDS before making payment – regardless of whether a VAT or PAN bill is involved.

| Payment Type | TDS Rate | Who Deducts |

| Contract / Service payment above NRs. 50,000 | 1.5% | The paying party (buyer) |

| Professional / Consulting fees | 15% | The paying party |

| Rent payment | 10% | The tenant / payer |

| Commission income | 15% | The payer |

| Salary / Wages | As per slab | Employer |

TDS is not a final tax – it is an advance payment toward the supplier’s annual income tax. The TDS deducted is shown as a credit when filing the annual income tax return. If TDS deducted exceeds your total tax liability, you can claim a refund from IRD.

Penalties For Not Issuing A PAN Bill

The Value Added Tax Act 2052 (as amended) specifies penalties for billing non-compliance. Even for PAN-registered businesses that are not VAT-registered, several penalties apply:

| Violation | Penalty | Legal Reference |

| Not displaying PAN registration certificate at business | NRs. 1,000 | Section 29(1)(Kha) |

| Not displaying tax notice board (Karpati) | NRs. 2,000 | Section 29(1)(A) |

| Not issuing any bill (PAN or VAT) to buyer | NRs. 10,000 per invoice | Section 29(1)(Ga) |

| Account books not updated or not maintained | NRs. 10,000 | Section 29(1)(Ma) |

| Not allowing IRD inspection or audit | NRs. 20,000 | Section 29(1)(9) |

| Operating a branch/warehouse without IRD approval | NRs. 10,000 per instance | Section 29(1)(ya1) |

| Preparing false bills or tax evasion | 10% of evaded tax + up to 6 months imprisonment | Section 29(2) |

Note: If your business is operating while your firm is VAT-suspended (non-filer status) and you continue to issue bills – that is treated as operating without registration, attracting the 10% penalty on the tax amount plus possible imprisonment under Section 29(2).

PAN Bill Vs VAT Bill – Key Differences

Understanding when to issue a PAN bill versus a VAT bill is essential for every business owner in Nepal. Here is a side-by-side comparison.

| Comparison Point | PAN Bill | VAT Bill |

| Who issues it | PAN-registered businesses NOT registered for VAT | VAT-registered businesses |

| Does it include VAT? | No – no VAT amount on the bill | Yes – 13% VAT added on taxable amount |

| Annual turnover threshold | Goods: under NRs. 50L and Services: under Rs. 20L | Goods: NRs. 50L+ and Services: NRs. 20L+ |

| Legal basis | Income Tax Act 2058 | Value Added Tax Act 2052 |

| Government purchases above NRs. 20,000 | Not accepted – VAT bill required | Required for all such transactions |

| Buyer can claim input tax credit | No | Yes – buyer can reclaim VAT paid |

| Bill format complexity | Simpler – no VAT calculation needed | More detailed – must show VAT separately |